Follow us for more exclusive content

Good debt: when it makes sense to borrow

In today's financial landscape, debt often goes with a negative connotation. High-interest loans, towering charges from a high interest credit card, and burdensome monthly payments can create significant financial stress. However, not all debt is created equal.

There exists a concept known as "good debt," which challenges the conventional wisdom surrounding borrowing. When used wisely and strategically, good debt can be a valuable tool for achieving financial goals and building a stronger future.

In this blog post, we will explore the circumstances where it makes sense to borrow, debunking the notion that all debt is inherently bad, particularly in the face of high-interest loans and mounting credit card debt.

Key Takeaways

- Debt is often associated with negativity, but there is a concept of "good debt" that can be beneficial when used wisely.

- Qualities of good debt include purposeful investment, being within budget, low interest rates, potential for growth, positive credit history, manageable debt-to-income ratio, and positive return on investment.

- Good debt examples include a mortgage (for home purchase), student loans (for education), and home equity loans (for home improvements or investments).

- Good debt is used to build wealth, improve finances, and achieve long-term financial stability.

Disclaimer

The contents of this article are for educational purposes only. They are not intended to be a source of professional financial advice. You will find experts on financial planning, financial management, and real estate here. More on disclaimers here.

Borrowing money

Borrowing money has become an integral part of modern financial management, allowing individuals and businesses to pursue opportunities, fund investments, and address pressing needs.

However, the concept of borrowing often carries a negative reputation, with concerns about high interest rates, debt burdens, and financial instability. While it's true that unwise borrowing can lead to financial hardships, it's important to recognize that responsible borrowing can also yield substantial benefits.

By understanding the intricacies of borrowing money and making informed decisions, individuals can leverage this financial tool to their advantage, creating opportunities for growth, stability, and achieving their goals.

Let's delve into the nuances of borrowing money, exploring the factors to consider and the potential benefits that can be unlocked through strategic borrowing practices.

How to use debt to make you rich

Many fear debt. Some take it on as an inevitable wrecking ball. Others who don't have the guts try to steer completely clear of it. But the wise and the rich have learned to use debt to their advantage. They've been doing so for decades and centuries.

According to some experts, individuals with a moderate net worth can employ "securities-based loans," where they borrow funds at a low cost from banks by leveraging the value of their investment portfolio as collateral. This method essentially enables them to loan money to themselves, as the portfolio's return on investment often surpasses the interest rate on the loan.

What is good debt status?

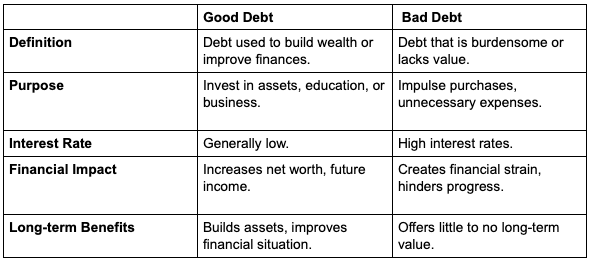

Debt can be categorized as either good or bad based on its purpose and impact. Good debt is used to build wealth or improve one's financial situation, such as investing in assets or education. It is seen as a strategic tool for long-term financial stability.

In contrast, bad debt refers to burdensome obligations with limited long-term value that can hinder financial progress. Differentiating between good and bad debt helps individuals make informed decisions and use debt responsibly to align with their financial goals.

What is a good debt level?

Typically, a favorable debt ratio ranges from 1 to 1.5, although the ideal ratio can differ across industries due to varying levels of debt financing. Industries with high capital requirements, such as finance and manufacturing, often exhibit higher ratios, which may exceed 2.

What is considered good debt?

Good debt refers to borrowed funds that have the potential to enhance your net worth or generate future income. These include loans taken to invest in a small business, education, or real estate, as these investments can contribute to your overall financial well-being.

It is important to note that good debt usually comes with a low interest rate or APR, typically under 6%, as recommended by experts. Good debts are worth more than they cost.

What are the qualities of good debt?

Good debt possesses several qualities that distinguish it from other types of debt. Here are some key qualities of good debt:

1. Purposeful Investment

Good debt is used to finance investments that have the potential to generate long-term value, such as starting a business, acquiring an education, or purchasing income-generating assets like real estate. It is a strategic financial decision aimed at improving your financial position.

2. Within Budget

Good debt aligns with your financial capacity and is within your budget. It is borrowed responsibly, considering your income, expenses, and financial goals. This ensures that the debt remains manageable and does not put undue strain on your overall financial well-being.

3. Low Interest Rate

Good debt typically carries a low interest rate or APR. This allows you to borrow money at a reasonable cost, minimizing the financial burden and maximizing the potential return on investment. A low interest rate helps ensure that the cost of borrowing remains manageable.

4. Potential for Growth

Good debt is often associated with investments that have the potential to grow in value over time. This includes investments in assets like a house, business, or education, which can increase your net worth or generate future income.

5. Positive Credit History

Taking on and responsibly managing good debt can help enhance your credit history. Timely payments and responsible borrowing habits contribute to a positive credit score, which can provide access to better loan terms and financial opportunities in the future.

6. Manageable Debt-to-Income Ratio:

Good debt should be structured in a way that keeps your debt-to-income ratio within a reasonable range. This ratio compares your total debt obligations to your income and helps determine your ability to manage and repay the debt. A manageable debt-to-income ratio ensures that your overall financial health remains stable.

7. Positive Return on Investment (ROI)

Good debt is expected to yield a positive return on investment. This means that the benefits and income generated from the investment should outweigh the cost of borrowing, including interest payments. The investment should contribute to your overall net worth and financial growth.

8. Long-Term Financial Benefit

Good debt focuses on long-term financial benefits rather than short-term gratification. It is an investment in your future financial stability and growth. The debt should align with your financial goals and contribute positively to your overall financial well-being.

9. Enhances Financial Position

Good debt has the potential to improve your financial position by increasing your net worth or generating future income. It helps you build assets, acquire valuable skills or knowledge, or enter into income-generating ventures. The goal is to strengthen your financial foundation and create opportunities for future financial success.

10. Prudent Financial Management

Taking on good debt requires careful financial planning and management. It involves evaluating the risks and rewards, considering your cash flow, and ensuring that you have a solid repayment plan in place. Prudent financial management helps mitigate potential risks and ensures that the debt remains beneficial to your overall financial situation.

It's important to note that while good debt can be beneficial, it still requires responsible borrowing and diligent financial management. Each individual's financial circumstances are unique, and it's advisable to consult with a financial advisor or professional to determine what constitutes good debt in your specific situation.

Good debt vs Bad debt

It's important to note that the classification of debt as good or bad can vary based on individual circumstances. These points serve as general guidelines to help differentiate between the two types of debt.

What is an example of good debt?

Good debt examples can include your mortgage, where you borrow money to purchase a home with the expectation that its value will increase over time. Additionally, there are potential tax benefits as you may be eligible to deduct the interest on mortgage debt from your taxes.

Good debts would typically be:

Student loan debt

Investing in education can lead to higher earning potential and career opportunities, making student loans a commonly considered good debt.

Home Equity Loan

If used wisely, a home equity loan can be considered good debt. It allows homeowners to borrow against the equity in their homes for purposes such as home improvements or investments. This type of debt can potentially increase the value of the property and contribute to long-term financial growth.

The following options are typically considered bad debts:

Auto loans

While auto loans (or car loan) may be necessary for purchasing a vehicle, they generally do not appreciate in value and can quickly depreciate. It's important to consider the overall cost and affordability before taking on an auto loan.

Payday loans

Payday loans often come with extremely high interest rates and fees, making them a form of predatory lending. They can lead to a cycle of debt and financial instability, so they are generally considered bad debts.

Personal loans

Personal loans can differ with respect to terms and interest rates. While they can be used for various purposes, they are not inherently good or bad debts. It depends on the specific circumstances and how the borrowed funds are utilized.

Personal loans for responsible purposes such as debt consolidation or home improvements may be considered good debts, while those taken on for unnecessary expenses or to cover overspending may be considered bad debts.

Consumer debt

Consumer debt refers to debts incurred by individuals for personal or household expenses. It includes debts such as credit card balances, personal loans, auto loans, payday loans, and other forms of borrowing aimed at financing consumer purchases.

Generally, consumer debts would be considered bad debt unless it is well managed.

It's worth noting that the classification of debt as good or bad can depend on individual circumstances and financial goals. It's important to evaluate each debt based on factors such as interest rates, potential for growth or improvement, and overall affordability before categorizing them.

How to manage debt

To effectively manage your debt and financial well-being, follow these tips:

Make timely payments

Monitor your credit regularly

Pay more than the minimum

Understand your credit limits

Evaluate your debt-to-income (DTI) ratio

Borrow only when necessary

Seek lower interest rates

Think twice before closing accounts

Build an emergency fund

By following these guidelines, you can enhance your credit profile, maintain financial stability, and make informed decisions about your personal finances.

What should I consider when taking on debt?

Evaluate the impact on your capacity to save for unforeseen expenses. If you're unable to establish a contingency fund, unexpected circumstances may lead to increased debt. Additionally, assess how it alters your debt-to-income ratio, as this could influence your access to credit during crucial times.

When it makes sense to borrow

So, when does it make sense to borrow?

When you're investing the funds in a business or in portfolios that yield higher interest rates than the debt interest rates. You should work with a financial advisor who can help you secure better investments and good debts.

Bay Street Capital Holdings

Headquartered in Palo Alto, Bay Street Capital Holdings is a prominent financial planning, wealth management, and investment advisory firm that places a strong emphasis on effectively managing total risk and volatility rather than solely focusing on maximizing returns.

Renowned for its commitment to diversity and inclusion, the firm's founder, William Huston, is recognized as one of Investopedia's Top 100 Financial Advisors for 2021, and Bay Street is one of only two Black-owned firms among the nineteen honored in California.

Notably, Bay Street actively supports diverse and emerging fund managers and entrepreneurs, showcasing its dedication to fostering inclusivity and opportunities.

In recognition of its exemplary practices, the firm was selected as a finalist in the Asset Manager for Corporate Social Responsibility (CSR) category, standing out among more than 900 firms nationwide in 2021.

Sources

https://www.wellsfargo.com/goals-credit/smarter-credit/manage-your-debt/tips-for-managing-debt/